Every time it comes to renewing your car insurance it can feel like your insurers have plucked a collection of numbers out of the ether to decide how much to charge you.

The metrics involved in calculating insurance premiums seem to be too vast for even insurers themselves to comprehend, but it turns out there are scores of esoteric factors that go into the mix in working out exactly how much to charge.

Wildly varying factors surrounding where you work, your location and even the weather can go into calculating the price of your premiums, catching many motorists off-guard. With this in mind, let’s take a look at seven of the more surprising reasons why your car insurance costs may go up:

1. Your Career Choice

Job discrimination appears to be rife in the world of insurance, and many insurers can link your premiums to your line of employment. For instance, if your profession will see you travel a lot as part of your job, you can expect to pay more for your car insurance. This can be bad news for delivery drivers, salesmen and journalists who might have to pay higher prices than receptionists, office workers or retail assistants.

Interestingly, jobs that can boost your premiums can involve highly stressful roles that can require more work and longer hours – resulting in a lack of sleep. Professions related to healthcare and finance could potentially fall into this category.

The reason why longer hour and stressful jobs are in the fold is down to the higher accident rates recorded among drivers who hold these high-risk jobs. This can potentially contribute to delivering high-cost premiums for otherwise safe drivers.

2. Your Credit Rating

Your credit rating can also have a major impact on your rate of car insurance. This can especially affect those who choose to pay their insurance monthly – with interest rates rising as credit ratings fall.

Although this may not seem like a surprising reason behind rising insurance premiums, each insurer uses its own systems to calculate your perceived credit rating. This means that some financial issues that were deemed insignificant elsewhere can cause a huge rise in premiums for other insurance companies.

This means that drivers looking to borrow to buy their perfect car may need to double-check how their insurance will look after accessing the credit they need to make a purchase. The same measures can go for using car finance platforms to compartmentalise car payments.

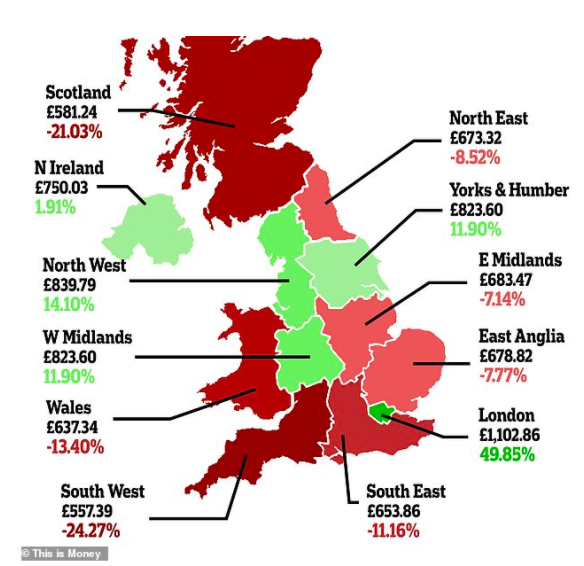

3. Your Postcode

Sadly, there’s a postcode lottery at play when it comes to insuring your car. While drivers in the South-West of England can enjoy over 24% lower premiums, London-based road users are faced with costs that range to nearly 50% higher than average.

While the trends surrounding locations and insurance premiums can vary, it seems that insurers favour more sparsely populated areas as opposed to more densely populated surrounds.

4. Your Relationship Status

Your personal life actually has a lot to do with your insurance premiums. Firstly, if your husband or wide intends to use your car too, you can add them as a named driver – spreading the risk of accident between two people.

If your partner has a good history of no claims, however, then it can actively bring the costs of your insurance down. However, adding a more experienced named driver with the sole purpose of bringing your insurance costs down is an illegal activity, which could come with criminal convictions.

Furthermore, having a child has also been known to bring your premiums down, with insurers assuming that this would prompt more responsible driving.

Sadly for singletons, those without partners or children may see the highest rates from insurers, due to companies linking a lack of dependencies with more reckless driving.

5. Your Neighbour’s Bad Driving

Here, the postcode lottery rears its ugly head again. If you relocate to an area that’s been shown to have a higher volume of accidents or crime, there’s a strong chance it will be reflected in your premiums.

If fact, theoretically, even if you remain in the same area and an accident black-spot emerges and prompts a higher volume of insurance claims, this can play a key role in affecting the costs of your premiums.

In the US, it was found that California car insurance premiums can fluctuate by as much as 33% depending on where drivers move to within the state – regardless of their ability and accident history.

6. Your Local Weather Forecast

Yep. Amazingly, the increasingly dire weather conditions year-on-year are forcing insurers to rethink their rates annually to account for the increased risks to the vehicles they cover.

Freak events are becoming more common over time, with wildfires, hurricanes, floods and blizzards prompting more claims in recent years. While in the UK we’re fortunate enough to enjoy relatively mild weather conditions compared to the US and Australia, for instance, more adverse weather during the winter months is not uncommon, and with the prospect of more accidents occurring on winter roads each year, more insurers will be looking to cover themselves by issuing heftier premiums.

7. Your Education

Another disappointing factor that could come into play when calculating insurance premiums revolves around your level of education.

US insurance comparison website, Jerry, has found that drivers who didn’t finish high school can expect to cough up over $3,300 more on average for their car insurance over the course of their lifetime compared to those who hold a degree.

Sadly, the world of car insurance isn’t fair. But through understanding some of the lesser-known factors that go into calculating your premiums, it may be possible for drivers to better set themselves up for cheaper rates.

Although we may not be able to change our level of education or our location, we can take steps towards building our credit scores and learning more about our local accident black-spots to mitigate our costs and get to the bottom of why some insurance quotes can be higher than expected.

The world of insurance can be a mysterious one at the best of times, but learning how insurers go about calculating their premiums is the key in working out how to get better coverage for our money.